Car Loans in Canada: Everything You Need to Know Before Financing a Car

Buying a car in Canada often requires financial assistance, and car loans in Canada are the most common way to finance a vehicle purchase. Whether you’re buying a new or used car, understanding car loans in Canada is crucial to making a smart financial decision. In this guide, we’ll cover everything you need to know about car loans in Canada, including interest rates, down payment requirements, and the pros and cons of financing.

Current Car Loan Interest Rates in Canada (2024)

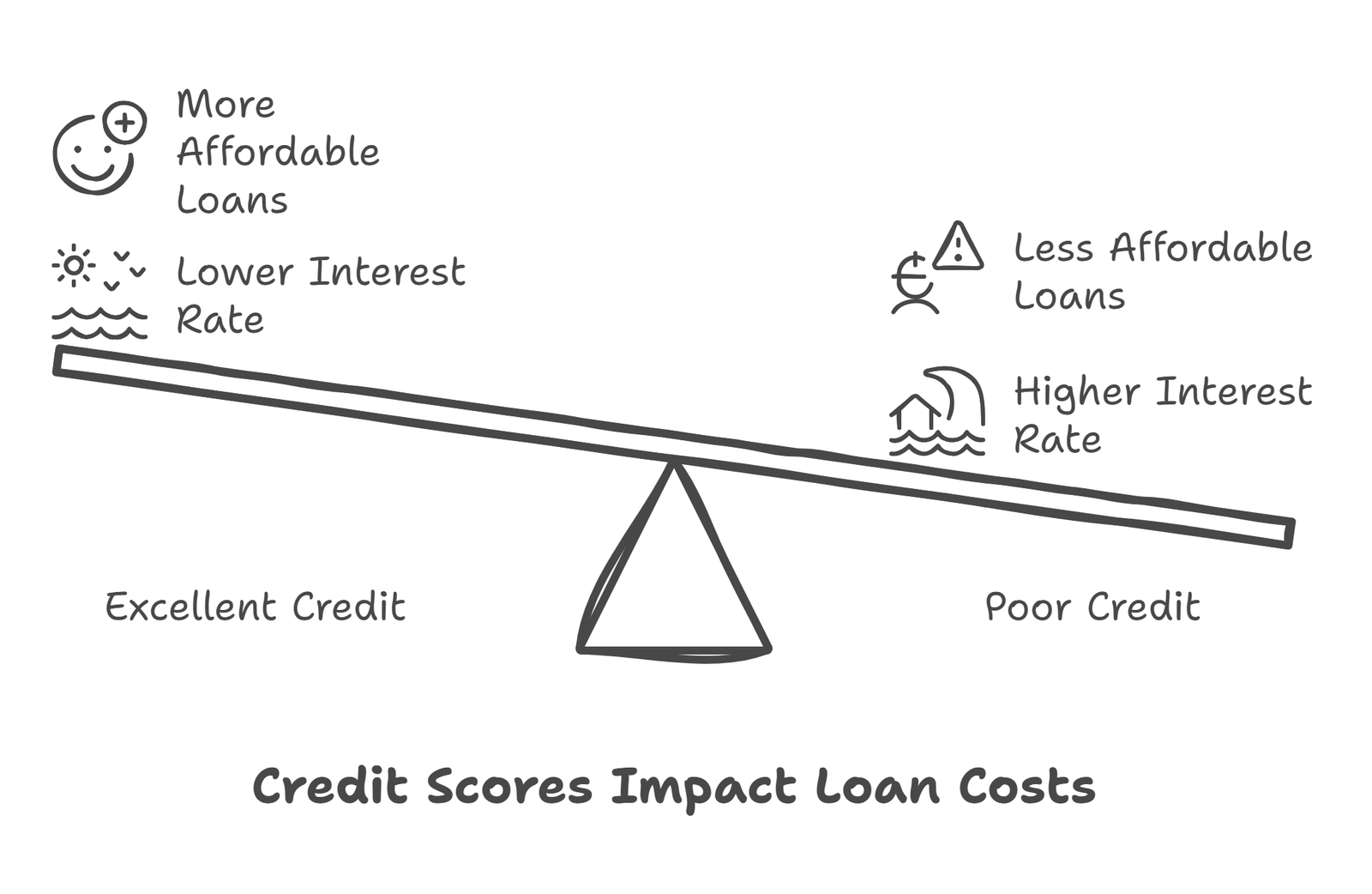

The interest rates for car loans in Canada depend on several factors, such as your credit score, the lender, and the loan term. Here are the average interest rates for car loans in Canada in 2024:

- Excellent Credit (760+): 5.99% – 7.99%

- Good Credit (700 – 759): 8.99% – 10.99%

- Fair Credit (650 – 699): 11.99% – 15.99%

- Poor Credit (Below 650): 16.99% – 29.99%

To secure the best interest rate for car loans in Canada, it’s important to compare offers from different lenders.

Down Payment Requirements for Car Loans in Canada

Most lenders require a down payment when applying for car loans in Canada. The typical down payment ranges from 10% to 20% of the vehicle’s price. Some lenders offer zero-down car loans in Canada, but these are usually for buyers with excellent credit. A larger down payment can reduce monthly payments and interest costs.

Car Loan Calculation Example

Let’s break down a real example of car loans in Canada to help you understand monthly payments:

- Car Price: $30,000

- Down Payment: $5,000 (15%)

- Loan Amount: $25,000

- Loan Term: 5 years (60 months)

- Interest Rate: 7.99%

Using a loan calculator, the estimated monthly payment for this car loan in Canada would be around $506 per month. Over five years, the total cost of the loan, including interest, would be approximately $30,360, meaning you pay $5,360 in interest.

Benefits of Car Loans in Canada

Taking out car loans in Canada offers several advantages:

- Immediate Car Ownership: No need to wait years to save up for a car.

- Flexible Loan Terms: Repayment periods range from 24 to 84 months.

- Credit Score Improvement: Making timely payments can boost your credit score.

- Access to Better Vehicles: Financing allows you to buy a newer, more reliable car.

Drawbacks of Car Loans in Canada

Despite the benefits, car loans in Canada come with some downsides:

- Interest Costs: The longer the loan term, the more interest you pay.

- Depreciation: Cars lose value quickly, sometimes faster than you can pay off your loan.

- Loan Approval Challenges: Those with bad credit may face high interest rates or rejection.

- Negative Equity Risk: If your car’s value drops below the loan balance, you may owe more than it’s worth.

Factors Affecting Car Loan Approval in Canada

Your approval chances for car loans in Canada depend on several key factors:

- Credit Score: A higher score means lower interest rates.

- Income and Employment Stability: Lenders check your ability to repay.

- Debt-to-Income Ratio: High debt may lead to higher interest rates.

- Loan Term: Shorter loan terms often have lower interest rates.

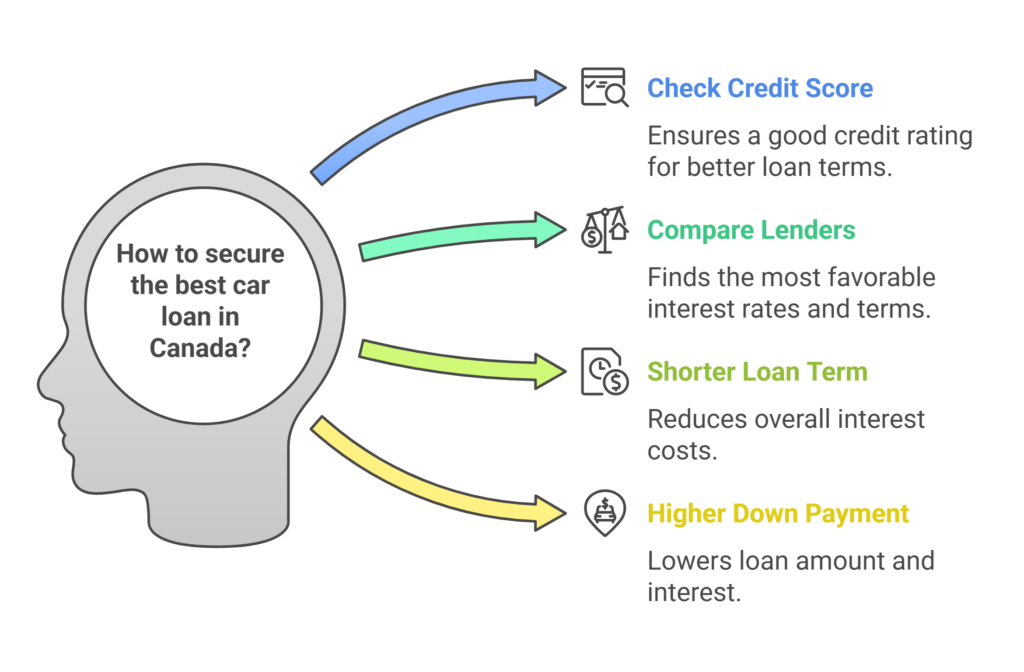

Tips for Getting the Best Car Loan in Canada

To secure the best car loans in Canada, follow these expert tips:

- Check Your Credit Score: Ensure it’s in good shape before applying.

- Compare Lenders: Don’t settle for the first offer—shop around.

- Consider a Shorter Loan Term: Reduces overall interest costs.

- Make a Higher Down Payment: Lowers your loan amount and interest.

- Negotiate Loan Terms: Some lenders may offer flexibility in rates and repayment.

Alternatives to Car Loans in Canada

If traditional car loans in Canada don’t work for you, consider these alternatives:

- Leasing a Car: Lower monthly payments but no ownership.

- Personal Loans: May offer better interest rates than car loans in Canada.

- Saving for a Larger Down Payment: Reduces the loan amount needed.

How to Get a Used Car Loan in Canada

Financing a used car is slightly different from financing a new one. Here’s a step-by-step guide to securing car loans in Canada for a used vehicle:

- Check Your Credit Score: Higher scores qualify for better rates.

- Set a Budget: Include the car price, interest, insurance, and maintenance.

- Compare Lenders: Options include banks, credit unions, dealerships, and online lenders.

- Get Pre-Approved: Helps you know how much you qualify for.

- Choose the Right Loan Terms: Shorter terms mean less interest paid.

- Make a Down Payment: At least 10-20% is recommended.

- Finalize the Loan and Buy the Car: Review loan terms carefully before signing.

By following these steps, you can secure car loans in Canada with favorable terms and drive away confidently.

Final Thoughts

Securing car loans in Canada is a great way to finance a vehicle, but it’s essential to understand the interest rates, down payment requirements, and loan terms. Always compare lenders, check your credit score, and consider the total cost of borrowing before committing to a loan. With the right approach, you can secure car loans in Canada that fit your budget while minimizing financial strain.

Are you planning to finance a car? Share your thoughts or ask questions in the comments below!

External Links (Authoritative Sources for Credibility)

- Government of Canada – Consumer Financial Education – Information on loans and financial literacy.

- Bank of Canada – Interest Rate Trends – Provides official interest rate updates.

- TransUnion Canada – Check Your Credit Score – Helps users understand their credit score before applying.

- Equifax Canada – Credit Reports and Scores – Another credit bureau for score checking

Also Read

10 Reasons Why BYD Cars Are Better Than Tesla Cars: A Comprehensive Comparison